The benefits of investing regularly

Regular investing by putting a set amount each month into a portfolio is a well-recognised approach to building wealth. Not only can it smooth returns, it can also take the hassle out of investing.

Makes investing accessible

Regular saving and investing is a great habit that can provide you with more flexibility further down the line. If you’re keen to begin investing but you don’t have a lump sum available, regular investing is a good way to slowly build up a pot.

Removes the worry about timing the market

It takes the emotion out of investing, as you don’t have to worry about when to enter the market, and just have to be confident that bad months will be outweighed by good ones over the long term. If you’re investing regularly, you don’t need to worry about trying to pick the right time to buy and sell your investments.

Smooth out market volatility

Rather than focusing on timing, if you routinely invest a regular amount over a period of time you will be investing across a range of prices. This averages the price of the investment, smoothing out the highs and lows in share prices. When they go up, the value of your stocks rise, and when they go down, your next contribution buys more.

Markets rise over time, just not every year

Markets do not rise every year, nor do stocks, even the best ones. This is because in the short term and maybe for extended periods, market levels and performance are not indicative of value. This makes it difficult for investors, who can find themselves oscillating between buying high (optimism or greed) and loss aversion, causing them to sell low (fear). In much the same way that diversification is a well-regarded investment approach as it is difficult to know which assets or sectors will be the strongest performers, cost averaging can be used to minimise the risk of buying or selling at the wrong time.

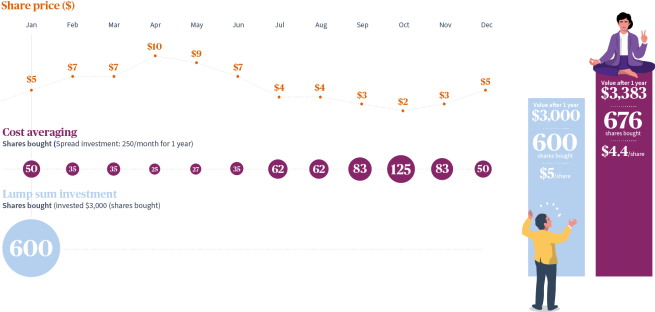

Cost averaging

Cost averaging is an investment strategy with the goal of reducing the impact of volatility on large investments. By dividing the total amount you are looking to invest into equal amounts, and investing at regular intervals, cost averaging aims to reduce the risk of incurring a substantial loss resulting from investing the entire lump sum just before a fall in the market.

The technique is so-called because it has the potential of reducing the average cost of shares bought. Cost averaging effectively leads to more shares being purchased when their price is low and fewer when the price is higher. As a result, it can lower the total average cost per share of the investment, potentially giving the investor a lower overall cost for the shares purchased over time. An example of this in practice can be seen below.

Please note that this strategy does not guarantee better results, as in a steadily rising market your investment could have benefited more from being made as an initial entire lump sum.

Drawbacks to this methodical approach

As can be seen in the example below, investors will miss out on the highest returns should the shares continue rising. The cost averaging strategy may trail a lump sum if this was purchased at a lower level. There are a couple more potential factors to consider – more frequent cost averaging trading could result in a higher level of dealing costs. It’s also important to consider what is being bought, as cost averaging in a poor-quality stock is of little benefit.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.