Market Outlook - Fixed income: Monetary policy should bolster markets

KEY POINTS

Fixed income markets should benefit from continued central bank easing in 2026. We expect lower interest rates in the US as policymakers respond to weaker labour market trends, and lower rates in Europe because of further declines in inflation. A resilient global economy and policy measures should keep fiscal concerns in check, allowing yields across the curve to reflect the growth and inflation outlook. The core scenario is positive for credit markets notwithstanding tight credit spreads and signs of increased leverage.

Central bank policy, as always, remains key to the bond market outlook in 2026. Major central banks are forecast to take short-term interest rates to or below estimated neutral levels in response to growth risks and falling inflation expectations. The International Monetary Fund’s recent growth forecasts were better than those made earlier in 2025 but still suggest advanced economies will struggle to meet long-term average growth rates in the years ahead.

That implies a more supportive stance from central banks as long as inflation remains close to targets. For next year, this suggests substantial reductions in US interest rates to below 3%. Additional US Treasury market yield curve steepening is likely to result. However, demand for yield remains strong, not least from the US insurance sector which has become a significant source of structural demand. Long-term yields are unlikely to significantly deviate from the trading range established in 2025.

Europe’s potential

The European Central Bank lowered its deposit rate to 2.0% in June 20251. Further cuts are possible should inflation undershoot the official target. This limits the potential for higher yields in European government bonds. However, once Germany’s ambitious spending programme gets underway there will be more supply of debt in the Eurozone’s biggest bond market, which could pressure markets at times. A steeper rate curve in the Eurozone is likely.

Outside of the bloc, the UK offers potential for attractive returns as markets only expect limited Bank of England easing. Lower inflation and tighter fiscal policy should drive UK gilt yields lower in 2026.

Despite this benign rate outlook, sovereign markets will remain at risk of increased investor concern on the fiscal side. The last year has seen government bond yields rise relative to equivalent maturity interest rate swap rates – a sign of increased risk premiums. Despite rate cuts, long-term yields have moved higher than their end-2024 levels.

The long-term trend for government debt levels is not encouraging in advanced economies, posing further scope for risk premiums to rise. However, the benign outlook for nominal growth and government attempts to take policy steps to appease bond market investors should limit any cases of ‘fiscal panic’. Steeper yield curves will at least offer investors potentially higher carry-driven returns in longer-duration strategies than has been the case for a while.

- European Central Bank, Key ECB interest rates, November 2025

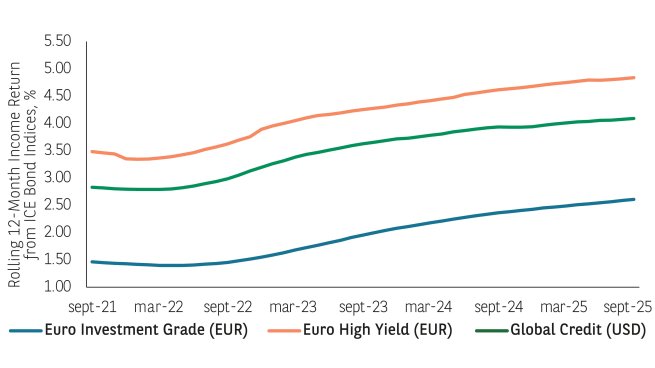

Credit bounce

Credit market activity has remained buoyant in 2025 with credit spreads narrowing over the course of the year despite elevated levels of issuance. Excess returns have been positive and underlying corporate fundamentals remain solid. Looking forward what will determine credit market performance is whether investors continue to value diversified exposure to corporate risk more highly than balance sheet-challenged sovereign debt. In which case, prevailing yields in credit markets are attractive and should deliver attractive income-driven total returns.

However, from a credit spread point of view, current valuations are tight, and the key risk is credit markets will experience periods of underperformance relative to government bonds. Catalysts for this are weaker economic data, equity market volatility or evidence of growing credit stresses in either private or public markets.

Geographically, US markets are most at risk from any deviation from the benign core scenario. Tariffs and the impact of immigration controls on labour supply could combine to keep inflation higher for longer. This not only complicates the Federal Reserve’s decision-making but also reduces expected real returns from US fixed income. It could also negatively impact the dollar. Any sense of increased politicisation of monetary policy (fiscal dominance) will tend to increase inflation expectations, steepening the US yield curve further and underpinning inflation break-even levels. If growth also turns out to be weaker, investors could also focus on the US fiscal outlook, again widening spreads in the US rates and credit markets.

In the absence of a growth or credit shock, carry will be a major theme for bond investors, delivering most of the total return. As such, high yield and emerging market bonds continue to be interesting from a total return perspective. Again, after a robust performance in 2025, investors need to be mindful of valuations but improved credit quality in high yield and better macroeconomic performance in emerging markets are positives for those markets. Significant drawdowns in fixed income markets tend to only occur in response to a growth or credit shock. Neither is in our core scenario for 2026 which means investors should be able to benefit from solid bond income returns.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.