What have you done for me lately?

Strong US earnings season results have helped US equity markets withstand negative news around the Iran war and relatively high oil prices.

Since Brent crude oil’s recent low of $99 per barrel on 17 April (the pre-war price was $71), prices jumped back up to $124 before dropping to $106 as at 14 May. Over that period, the S&P 500 rose by 5.3% while the MSCI World ex-USA index fell by 0.6% (in local currency terms).

With the earnings season behind us, however, markets may struggle to find good news to offset less positive reports from the Middle East. For the US, economic data may be the source.

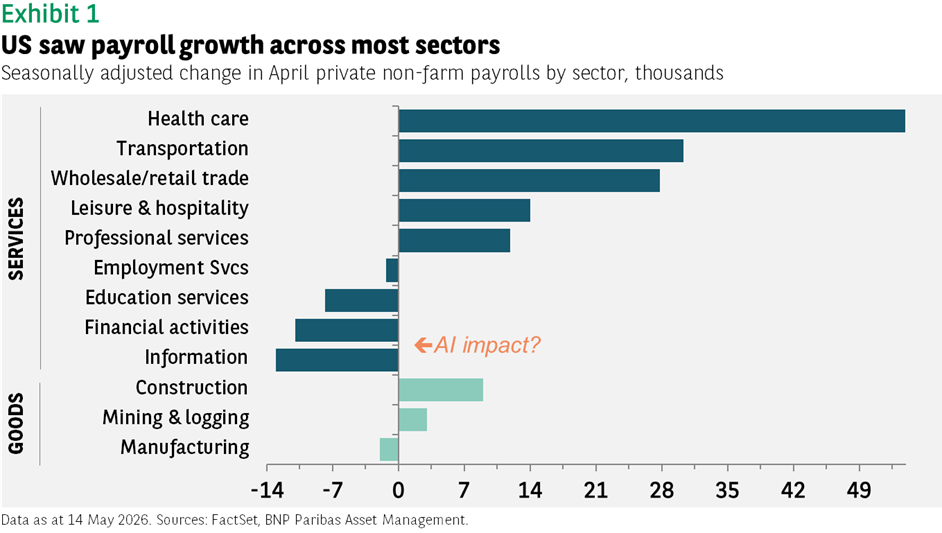

US non-farm payrolls showed another month of reasonably strong job creation in April. It has been noted that healthcare once again accounted for the largest share of the gains, but robust job creation in the sector has been the norm for decades as the US population ages. More meaningful were the gains across other parts of the labour market (see Exhibit 1).

Declines in the Financial activities and Information sectors were taken by some as a sign of artificial intelligence-induced job destruction. Given the news headlines about corporate layoffs, there is probably some impact from AI but it seems unlikely that it is significant at this point. Professional services employment still grew, and the losses in Financial activities were concentrated in the (slow moving) insurance sector, while Information declines mostly come from the motion picture industry.

With the adult unemployment rate steady at under 4%, and wage growth improving, the US labour market seems solid for now, which augurs for steady consumer demand in spite of high petrol prices. April’s core retail sales figure, which showed a 0.5% gain on the month, supports this view.

A diverging economic backdrop in Europe and Asia

Europe, by contrast, is at risk if the Strait of Hormuz remains closed and declining oil inventories lead to another spike in prices. Recent economic data has been less encouraging than in the US.

Service sector Purchasing Managers’ Indices declined across most major European countries in April, either moving from expansionary to contractionary territory or falling further into contractionary territory. US services PMIs were steady or improved and showed the sector expanding.

The diverging economic backdrop has been reflected in the performance of European equities this year compared to the US as measured by the Russell Value index, which shares a similar sector makeup.

Until the outbreak of war, returns were similar: both were up 7% by the end of February. Since then, European equities have fallen 3% while US value stocks have gained 4%.

China (and Asia in general) is also more exposed to the crisis than other regions. Credit growth in China has slowed, and PMIs are only slightly in expansionary territory. Exports have been the economy’s saving grace, but this is unlikely to be a sustainable strategy.

Countries on the receiving end of the flood of cheap Chinese imports increasingly worry about their own industrial base and may well increase trade restrictions in the future.

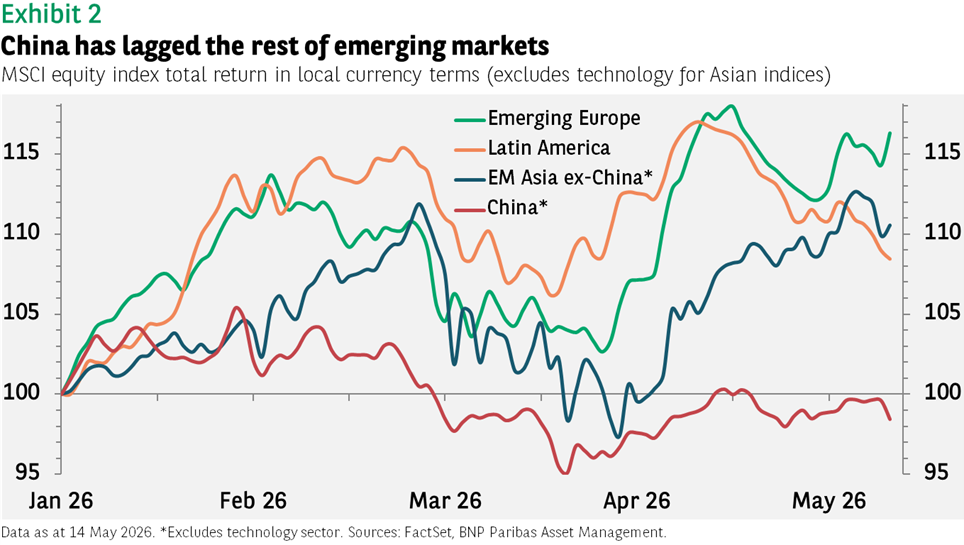

The Iran war, though, has arguably only exacerbated problems in what was an already weak economy. Chinese equities (excluding technology) have underperformed the broader emerging markets universe for the whole of the year to date (see Exhibit 2).

The gap for the technology sector is even larger. While Taiwanese and Korean tech shares are up 58% and 157% year to date, respectively, in China they have dropped by 12%.

Investors in the country’s equities will hope that the recent China-US summit results in some meaningful improvement in the relationship between the two superpowers.

Performance data/data sources: FactSet, BNP Paribas AM, as of 14 May 2026, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of BNP PARIBAS ASSET MANAGEMENT Europe or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.