Why market turbulence has created opportunities for European credit

Key points:

- Despite recent economic turbulence, the euro credit market offers investors unique opportunities with nearly 5% yields for a 4.5-year duration.

- European corporates have displayed resilience despite macroeconomic challenges, and default rate should remain within historic averages.

- Technicals should remain a positive contributor due to healthy inflows and well-absorbed supply.

Despite a turbulent macroeconomic landscape which has unfolded over the past 18 months, we believe investors enjoy a unique position to take advantage of the current market conditions. Previously, the strong involvement of central banks had suppressed spreads and volatility through massive quantitative easing programs. However, 2022 marked a shift, as the global financial markets collapsed in one of the most turbulent years:

- the war in Ukraine brought a massive and historic energy shock to the markets;

- the weaker macro background, especially in China, led to depressed growth outlook;

- this was combined with rampant inflation as global economies broke out of the pandemic with strong demand and constrained supply.

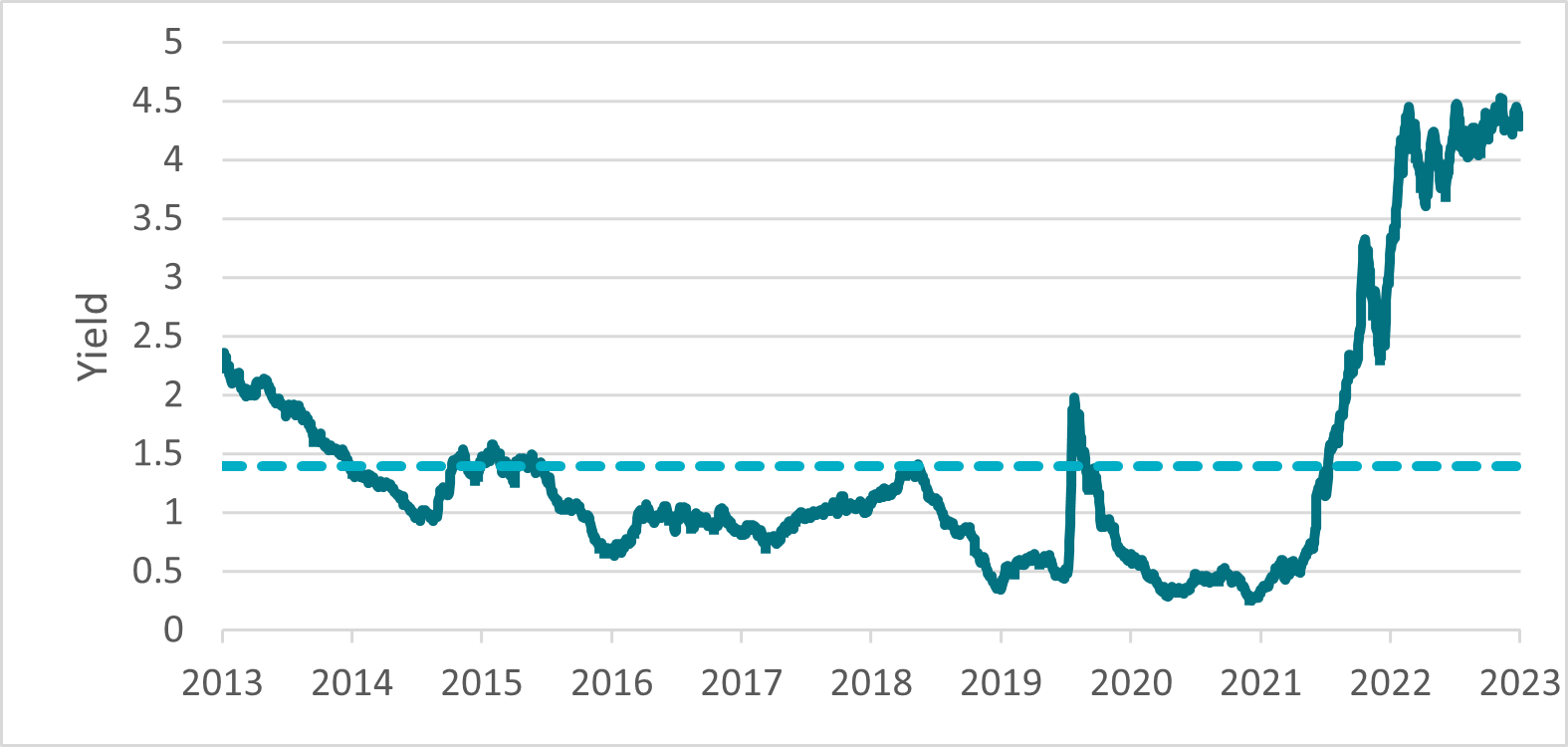

These factors led to stickier inflation and weaker-than-expected growth. Central banks conducted some very aggressive monetary policy tightening with 10 straight interest rate increases from -0.50% pre-2022 to 4% in September 2023. This obviously created some volatility in the rate markets, pushing yields and spreads higher. Today, the euro credit market offers nearly 5% yield for a duration of 4.5 years, the highest level over the last decade. This high level of yield and higher-for-longer monetary policy is likely to remain in place for at least the reminder of the year, which ultimately is offering attractive opportunities for investors in the euro credit market.

Historical Yields for Euro Credit IG index

Source: AXA-IM, Bloomberg, as of 31/08/2023. Euro Credit IG index refers to ICE BofA Euro Credit Index

European companies evolving in a softer macro environment

In 2022, there was a lot of concern about the health of European corporates and financials. The markets were troubled by companies who had to face the effect of inflation and weaker economic activity. Surprisingly, European companies have remained resilient despite a decelerating momentum:

- revenue growth softened in 2023 but continued to be in positive territory;

- leverage has remained flattish and did not deteriorate significantly;

- and interest rate coverage remained at high levels due to strong starting point.

In Financials, banks have benefited from good volumes growth and higher interest rate environment. Despite rising rates, the quality of assets has improved vs pre-pandemic levels and most banks are expecting a normalisation in the cost of risk guidance for the coming quarters.

From a high yield perspective, we have seen an increase in the default rate of around 2% in Europe. We expect this default rate to increase in the coming quarters to about 4% and in line with historical average.

Overall, the fundamentals continue to reassure us on the resilience of European corporates and financials. In this current environment, we have a preference for Financials given robust fundamentals for banks. In Corporate, we avoid some sectors like Chemicals, Retail and Capital Goods given tight valuation and weaker fundamentals. In terms of capital structure, subordinated debt continues to offer attractive carry to portfolios.

Outlook for European credit

The gradual process of tightening by central banks in developed markets is nearing its conclusion. The discussion now revolves around how long interest rates will remain at higher, restrictive levels, and there is a concerted effort to resist premature rate reductions. We anticipate modest changes in the near future, neither significant improvements nor substantial declines in the credit market. Within the investment grade segment, companies are sitting tight on the low coupons they locked in during the cheap-money era, pushing out maturity walls. These issuers have had ample time to adjust to the gradual market conditions, resulting in a heightened emphasis on reducing debt burdens rather than pursuing extensive M&A initiatives.

From a technical perspective, we have seen strong inflows from Insurers and Pension Funds mostly due to the attractive yield on the duration. We expect this trend to continue as we are seeing a lot of traction within the credit market. Supply on the other hand has increased by nearly 20% since the beginning of the year with above to €430bn of gross issuance

In general, corporates had been quite opportunistic and they have built up substantial cash reserves on their balance sheets. As a result, they won't need to seek additional funding in the near future. Similarly, financial institutions have already tapped the market extensively since last year, and their issuance is expected to remain limited for some time. Consequently, aside from those issuers requiring capital for green transition initiatives or for regulation purposes, most players in the market won't have an immediate need to raise funds. This dynamic should contribute to sustained high demand in the euro credit market, which we view as a positive development.

In this context, we believe active euro credit strategies can benefit from such an environment. In particular, total return credit strategies should be able to take advantage of attractive entry points especially from a yield perspective, as well as bring resilience through their unconstrained approach and flexible positioning.

References to companies and sector are for illustrative purposes only and should not be viewed as investment recommendations.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.