Multi-Asset Investments Views: Fed up with dots

KEY POINTS

The Federal Reserve’s (Fed) December meeting provided investors with an updated narrative that cut short expectations for a Christmas rally, shook sentiment and stirred positioning. The reduction of Fed Funds Rate by 25 basis points came as no surprise and once again, the ‘dots’ - indicating where Fed Board members saw the path ahead for rates - were revised up, marginally higher than expectations. Add to that Cleveland Fed president Beth Hammack’s dissenting vote to keep rates steady, and markets sold off across the board taking yields higher, credit spreads wider and equities lower.

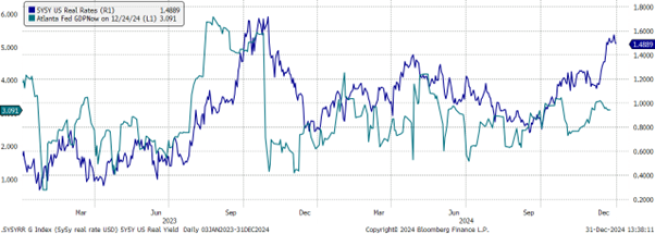

There was little cushion in the pricing of the US Treasury market for any disappointment regarding the policy outlook. Market positioning ahead of the Fed meeting was heavily tilted toward risk, yet markets were thin with lighter trading volumes in December, so potentially more volatile. Having been a splendid year for risk, some profit taking and risk reduction was expected as uncertainty around policy is gradually priced back in – the chart below shows the evolution of the Five-Year, Five-Year US Treasury Real Yield (that is, the yield on a five year Treasury starting in five years’ time) with the Atlanta Fed Nowcast for US GDP. The Fed has also indicated that it may not continue to cut rates at the pace it has set since the start of the cycle.

All in all, the backdrop to growth led by the US is still very much supportive. In fact, history appears to show that central banks generally end up cutting below their neutral rate more often than not and that this is exacerbated when unemployment starts to rise - exactly as the Fed has indicated thus far.

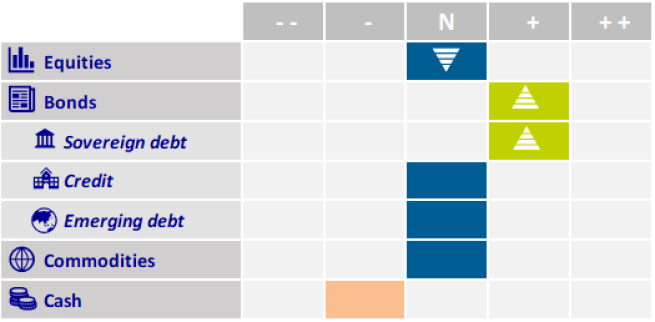

Our Macroeconomic Research team expects above-consensus US GDP growth in 2025 and while valuations are elevated, they have not yet reached exuberant levels. Our machine-learning-driven Bull/Bear model, which has historically provided accurate and timely warnings of major turning points, continues to offer reassuring signals. This model suggests the current bull market is not over, though it is now more than two years old. However, the December re-pricing in US rates (with markets expecting a less generous Fed) has moved us back into the multi-asset ‘danger zone’ of positive equity-bond correlation or US 10-year yields in excess of 4.5% - where the level of yield changes expected by markets can negatively impact the current valuations of risk assets, as we witnessed last April and several times in 2022. We have decided to be patient and have trimmed our equity exposure to neutral.

As bond yields climbed higher, the market experienced renewed bifurcation. Long-duration assets and small-cap stocks have recently underperformed large-caps, with industrials and bond proxies like homebuilders facing additional headwinds amid rising borrowing costs. Meanwhile, large-cap growth stocks, particularly in technology, showcased resilience, benefiting from robust earnings and their perceived defensive characteristics against a backdrop of policy uncertainty. Beyond these, US banks have failed to benefit from the rise in yields, instead correcting lower alongside the broader market. We believe this move is exaggerated, as factors such as increased deregulation, expectations for higher merger and acquisition activity, and rising yields should all provide support for the sector. We particularly favour US financials.

In this later stage of a maturing bull market, we prefer quality and low-volatility stocks. Additionally, the divergence in growth and fiscal policies between the US and Europe strengthens our preference for US equities. The potential implementation of US protectionist measures further supports an overweight stance on this market. That said, we continue to closely monitor sentiment and positioning in European equities, as their historical underperformance suggests potential for a rebound.

Hammack cited concerns over US inflation to justify her dissenting vote at the December Fed meeting, but the core Personal Consumption Expenditures index, released after the meeting, actually surprised to the downside. Since then, the US Treasury curve has stabilised and started to steepen again, which should help build some term premium into longer maturities representing a healthier market environment. In the rates markets, duration is looking increasingly attractive, especially in core Eurozone bonds which suffered over the quarter from rising US bond yields.

We also remain positive on gold as a diversifier. Although higher yields are typically seen as a headwind for gold prices, we anticipate that the Fed will continue normalising monetary policy through rate cuts, which should support higher gold prices. Additionally, potential inflationary pressures from new policies under Donald Trump’s administration could drive gold prices higher. Meanwhile, physical demand for gold appears to be strong despite the significant price increase over the past year. We expect central bank purchases to continue supporting gold prices, as countries remain cautious of sanctions and seek to diversify their holdings, which are predominantly in US dollars.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved

Image source: Getty Images

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.