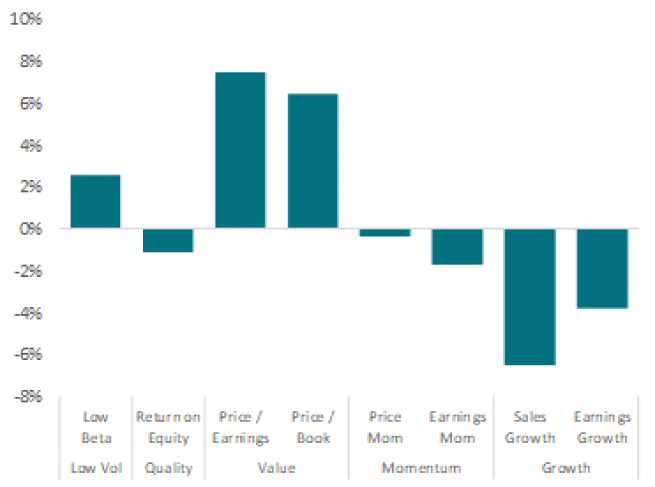

Global Factor Views: Positive on ‘Quality’ equities

- Global growth continues to feel the pressure in the current macroeconomic environment

- The central bank tightening cycle is mostly priced in, limiting further bond yield upside

- Equities are looking cheaper in relative terms, and we presently favour 'Quality' stocks

The Ukraine war continues to pose a material supply-side shock, driving inflation higher and slowing post-pandemic growth. Given the present backdrop, we forecast global growth to rise by 3.1% this year and 2.8% in 2023.

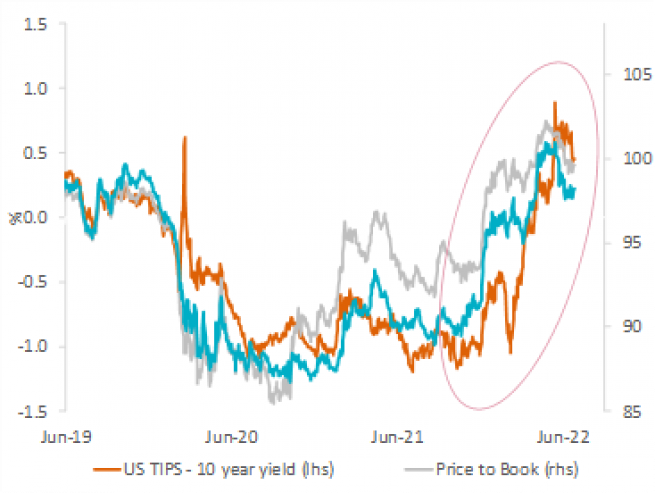

Inflation has not yet peaked, and most central banks will continue to raise interest rates and tighten policy, although much of the anticipated tightening is now priced in, limiting further bond yield upside. In our view equity valuations now look reasonable but not cheap.

However, given where we are now - elevated inflation and risks to growth - we anticipate that corporate earnings will come under pressure in the coming months and as such we advocate caution for the rest of 2022.

Given the present environment, we outline our outlook for equity market factors below:

Quality: Positive

Quality - i.e. companies with more consistent earnings and typically less share price volatility - did not deliver its normal level of defensiveness during the market correction during the first half of 2022.

This is chiefly because of its lack of oil exposure and because ‘quality growth’ de-rated, as real interest rates (taking inflation into account) rose.

However, we remain positive on Quality stocks because we do not expect significant further increases in real yields - bond interest payments after accounting for inflation - meaning the de-rating headwinds experienced by ‘quality growth’ is likely to be behind us.

Furthermore, corporates face a slow growth or even recessionary macroeconomic outlook, and earnings growth is likely to slow. As such, we believe investors will favour - and may even pay a premium for - companies with a proven track record of earnings growth or which are beneficiaries of secular growth trends, such as the transition to a clean economy.

Low volatility: Neutral

The Ukraine crisis has added to inflationary pressures but damaged global growth expectations and investor risk appetite, leading to a sharp equity market correction.

Against this backdrop, it should come as no surprise that lower volatility stocks - those which in relative terms generally experience lower levels of volatility - outperformed the market in the first half of the year.

A slow growth or even recessionary macroeconomic outlook continues to argue in favour of the defensive attributes of the style. However, we remain neutral because Low volatility price-to-earnings (P/E) multiples are relatively elevated, and the style would likely underperform sharply in a scenario where macro conditions surprise on the upside.

Value: Neutral

We moved overweight Value in January (maintaining that position despite the outbreak of the Russia-Ukraine war) because rising real rate expectations favoured short duration stocks and Value – stocks which appear to be trading for less than their underlying value - was cheap.

But we have downgraded our outlook for Value to neutral because we do not expect further significant increases in real yields and the outperformance of Value this year means that the valuation gap between Value and Growth has normalised.

We remain neutral as the current uncertain macro and geopolitical outlook still argues in favour some ‘defensive value’ sectors and, while Value is no longer relatively cheap, neither is it relatively expensive.

Momentum: Negative

Price momentum as a factor captures stocks that have a positive price change, relative to the market, over the last 12 months.

Currently price momentum is correlated with low volatility and defensive areas of the market. We would prefer to obtain defensive exposure directly and as such recommend an underweight position in price momentum to avoid over-exposure to a scenario where macro conditions surprise on the upside and markets sharply reverse.

With a more demanding outlook for corporate earnings, our preferred measure of investor sentiment continues to be the momentum of near-term earnings revisions.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.