US reaction: Services inflation makes pivotal shift lower

- 11 July 2024 (5 min read)

US CPI inflation surprised to the downside in June. Headline inflation dipped by 0.1% on the month compared to an expectation for a 0.1% rise, seeing the annual rate drop to 3.0% from 3.3% (3.1% expected) - the joint lowest rate since March 2021 (along with last June). The core rate, excluding fuel and energy, also came in softer than expected, rising by just 0.1% on the month compared to expectations for 0.2%. The annual rate slowed to 3.3% (from 3.4%) also the lowest reading for over three years.

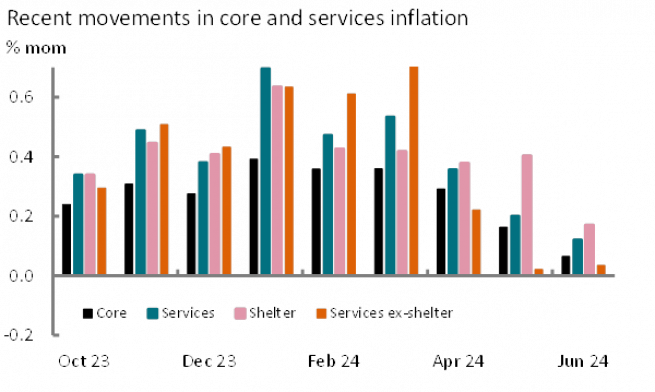

The fall in headline inflation was once again helped by a sharp fall in gasoline prices, motor fuel as a whole down 3.7% on the month. This helped broader commodities inflation to post its fourth consecutive monthly fall with only one month in the last 12 showing prices increases. Annual commodity price inflation is currently -0.4%. However, the Federal Reserve (Fed) has been focused on services inflation, which has been more persistently sticky and is more directly impacted by domestically generated inflation pressures, rather than the unwind of exogenous pressure including supply chain concerns. Annual services inflation has eased back in recent months and stood at 5.0% in June. While still elevated in annual terms, this understates the softening in recent months, with June’s monthly rise up just 0.12% - the smallest since January 2021 – following 0.36% in April and 0.20% in May. The composition of June’s services inflation also looks pivotal (Exhibit 1). While services ex-shelter posted another small rise in June, up just 0.04% after May’s 0.02%, shelter inflation appears to have finally cracked. This recorded a rise of just 0.17% having averaged a pace of 0.45% over the past 14 months. We have been expecting to see the drop recorded in new rents elsewhere feed through to the existing rents component of shelter inflation, but considered this only likely in H2 2024 as the six-month sampling of this series took effect. This looks like it has now emerged and we expect the coming months’ shelter inflation to be similarly subdued.

Fed Chair Powell reiterated at this week’s semi-annual monetary testimonies to Congress that the Fed required more evidence to gain sufficient confidence of softening inflation to ease monetary policy. However, at the June Fed meeting he had described May’s inflation data as “good”. June’s is better. With the Fed Chair also describing the labour market as “balanced” and displaying signs of “cooling” the Fed appears to be presented with inflation data that are becoming more benign and a softening in the labour market. We suggest that given the economic evidence, market pricing of <5% chance of a July cut appears stingy. In practice, with Powell remaining cautious just day’s earlier the Fed has laid the groundwork for a hold in July and there is little out between now and the Fed’s meeting on 31 July to scare them into an earlier move (the first estimate of Q2 GDP will be consequential, but expected at around 2% we do not expect it to precipitate a hurried reaction). As such we are comfortable with our view that the Fed will begin to ease policy only in September and still consider two hikes this year, penciling in a further cut in December.

Markets reacted predictably to today’s softer than expected inflation. The probability for a September cut rose from around 70% to just below 90%. Markets now price the chances of more than two cuts this (only around 15%) for the first time since early April (from only seeing an under 90% chance of two cuts). Longer-term yields followed the move, 2-year US Treasury yields down 14bps to 4.49% and 10-year yields and 10-year yields down 10bps to 4.18% - its lowest level since March. The dollar also softened dropping by 0.6% against a basket of currencies on the release.

Related articles

View all articles

Ca reaction: BoC cuts again, Fed outlook provides free reign

- by David Page

- 04 September 2024 (3 min read)

US reaction: Powell speech – getting into a hole?

- by David Page

- 23 August 2024 (3 min read)

UK reaction: Confirmation for the Bank of England

- by

- 14 August 2024 (5 min read)

US reaction: Inflation slowing in line, but nothing weaker

- by David Page

- 14 August 2024 (3 min read)

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© AXA Investment Managers 2024. All rights reserved