EU Taxonomy: Six key questions on the new flagship climate rules

What is it, and why is it needed?

The EU Taxonomy is a new European Union regulation. It is effectively a list of business activities which companies and investors can legitimately claim are ‘climate-friendly’. Ultimately, this should allow investors to make more informed and consistent comparisons between companies, based on the share of Taxonomy-aligned activity in their day-to-day operations.

In the field of green and sustainable investment great progress has been made in the collection and analysis of data that relates to environmental, social and governance (ESG) factors. This has helped us to build investment products that can assess companies according to ESG risks – including climate risks – as well as identifying businesses with the potential to contribute to a low-carbon future.

Still, there has remained a lack of firm, agreed criteria in the financial world for how to decide whether activities are genuinely contributing to a future net-zero economy. Over time, we expect the EU Taxonomy will help fill that gap, as well as tackling ‘greenwashing’ – where environmental ambitions and language are not matched by actions and outcomes.

How does the Taxonomy work?

The EU Taxonomy is a mandatory regulation, but only in terms of the disclosure of Taxonomy-aligned revenue and capital expenditure. There is no systematic compulsion for a company to increase the share of aligned activities, or for an investor to favour a company with a higher relative share.

The Taxonomy is designed to work alongside two other disclosure-based regulations: The Corporate Sustainability Reporting Directive, which combines social and environmental factors and will apply to all listed companies; and the Sustainable Finance Disclosure Regulation (SFDR),

For an activity to be termed as ‘Taxonomy-aligned’ it must make a substantial contribution to one of the six EU environmental objectives set out below – and do no significant harm to any of the other five. Detailed descriptions of what those terms mean for each objective are set out in the text of the regulation. To qualify, an activity must also meet minimum social safeguards and comply with the technical screening criteria.

How is the ‘substantial contribution’ decided?

The full text of the regulation sets out specific examples of what constitutes ‘substantial’ for individual business activities. But generally speaking, they must be aligned with carbon neutrality, and with limiting the increase in global temperature to within 1.5°C of pre-industrial times.

This may mean that an activity has a low impact on the environment as well as the potential to replace high impact activities, such as renewable energy. It may also reduce the impact from other activities, as in the case of wastewater treatment, or it may make a positive environmental contribution, for example the restoration of wetlands that can act as a carbon sink.

The regulation identifies two specific types of activity that may indirectly meet the ‘substantial’ test. Some operations are deemed transitional activities that thus far have no viable low carbon alternatives, but which are proven to be best-in-class in the relevant industry. Such activities would only be eligible if they do not hold back those low-carbon alternatives, and do not ‘lock-in’ carbon intensive assets. Other businesses may be deemed to offer enabling activities which contribute to the delivery of substantial effects elsewhere, such as a manufacturer building wind turbine blades.

How is the Taxonomy being rolled out?

Although the Taxonomy Regulation formally went live in July 2020, the first disclosures were not required until January 2022, and applied initially only to the first two of the objectives set out above. Mandatory reporting for the remaining four objectives is due to come into force in January 2023.

At first, the Taxonomy covers the economic activities of about 40% of listed companies, in sectors which are responsible for almost 80% of direct greenhouse gas (GHG) emissions in Europe.

Early estimates from the European Commission for the potential alignment of company activities and investment portfolios emphasised this sense of evolution. It said that alignment would tend to fall in the range of just 1% to 5%, but that the figure was expected to “rise significantly” with the implementation of the EU Green Deal – the set of policy initiatives put in place to support the goal of reaching net zero by 2050.

How does the Taxonomy treat fossil fuels and nuclear power?

This has been a source of some controversy as the regulation is formed. Although coal and oil of all forms cannot be classified as Taxonomy-aligned, the European Commission published a text in February 2022 that proposed allowing nuclear and gas to be included “under clear and tight conditions”. This is based on their classification as transitional activities, the category originally reserved for sectors without viable alternative technologies in place, such as cement production. This text will be scrutinised by the European Parliament and Council of Member States over the coming months but is very likely to be adopted.

Some investor groups felt the inclusion of nuclear and gas could affect the credibility of the Taxonomy. However, both are considered as intermediate sources of power that can smooth the path to net zero as the world reduces its reliance on more carbon-intensive energy sources. The Commission sought to address the concerns by introducing more stringent disclosure requirements on nuclear and gas operations, including a requirement for third party verification.

More broadly, oil and gas firms can still be credited for Taxonomy-aligned activities and investments. If a major energy company sharply increases the share of its revenues derived from solar power, for example, this will be reflected in its Taxonomy disclosures and allow investors to compare its progress to peers.

How will AXA IM prepare its EU Taxonomy disclosures?

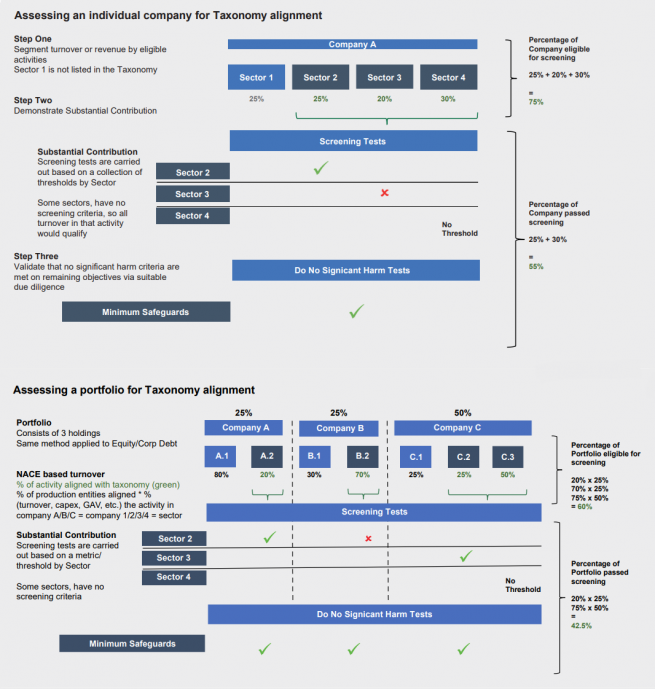

This process will evolve over time, but we can already see how the Taxonomy has provided a structure for investors to better evaluate assets and portfolios. Our three-step approach for individual companies is to first identify the portion of revenues derived from activities which may fall in the scope of the Taxonomy, and then apply the substantial contribution test to those activities, before finally assessing whether they do no significant harm to the remaining objectives. That would give us a final percentage of the company’s activities that are Taxonomy-aligned.

This process can then be expanded out to the portfolio level and will give us the ability to provide clients with a full assessment of Taxonomy-aligned exposure across all six of the EU environmental objectives. The graphic below from the EU’s Technical Expert Group offers a hypothetical walk-through of that process using a simplified example.

As with many aspects of this evolving legislation, our reporting of Taxonomy-alignment will expand and adapt over time. As an example, however, for strategies that consider environmental objectives under the most stringent ‘article 9’ classification in the EU’s SFDR, we report Taxonomy-alignment in the 2021 annual report of the funds. We will then report Taxonomy alignment within SFDR periodic reporting from early 2023, as well as in the ESG Report for article 8 and 9 strategies from that date.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments .and the income from them can fluctuate and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.