Hydrogen and the energy transition: One molecule to rule them all?

-

Hydrogen is not a climate change silver bullet, but it can be a credible part of the strategy to decarbonise our energy system, if it is itself produced without carbon

-

The objective should be to develop a hydrogen ecosystem, built around green hydrogen. This will require investments in transport and storage infrastructure

-

We argue that opportunities for investors arise more in renewable electricity and integrated hydrogen supply chain areas than in equipment suppliers

The Intergovernmental Panel on Climate Change (IPCC) made clear in its August 2021 report that humankind is making a dramatic contribution to global warming through emissions of greenhouse gases, mostly carbon dioxide (CO₂) and methane (CH₄).

Right now, and despite increasing efforts from governments, businesses and investors, we remain locked in the fossil fuel-based economy that has powered our world since the industrial revolution. Coal, crude oil and natural gas – which together account for about 80% of emissions – have offered us high energy density and relative ease of transport and storage.

As our economies and societies transition, we will pay higher prices as the cost of carbon is made visible. In economist lingo, we will internalise an externality. Living with two energy systems as we transition will be an additional source of costs, but there are investments and growth to be found in this transition too.

It is also a behavioural and social transition. We will have to make hard choices on what we consume and redefine ‘basic’ and ‘luxury’ habits. The logic of on-tap availability of energy, goods, and services could be questioned, at least in rich countries with high emissions per capita.

In this context, hydrogen – to be precise, di-hydrogen or H₂ – has gained prominence in recent years among the many tools, levers, and broad solutions that can be used to decarbonise.

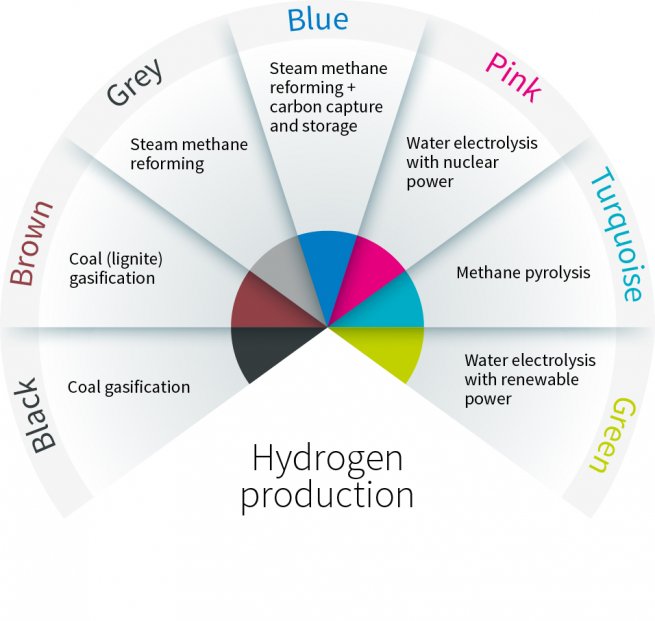

Grey area

The hydrogen economy already exists. About 90 million tonnes (MT) was produced in 2020 according to the International Energy Agency (IEA).

But the buzz around hydrogen is really about so-called ‘green’ hydrogen – produced through the electrolysis of water, using renewable electricity. In such a production pathway, there are no CO₂ emissions. According to the IEA, however, green hydrogen accounted for a paltry 0.03% of total production in 2020.

In all energy transition scenarios, the hydrogen market is expected to grow – from doubling to multiplying sixfold by 2050 – as hydrogen is deployed in markets beyond its current applications, and as the cost of green hydrogen declines drastically. Greater scale will contribute to cost reduction, as will an expected steady reduction in the cost of renewable electricity and the proper industrialisation of the electrolyser industrial chain.

Current cost projections forecast green hydrogen to become cost competitive in a decade or so. If a cost of carbon is added, ideally globally and at a high enough level, this would further enhance the relative attractiveness of green hydrogen by making grey hydrogen dearer.

Hydrogen could also join the debate about the need for strategic metals in the energy transition. There are two dominant electrolysis technologies – alkaline and proton exchange membrane or PEM – and they require large quantities of nickel and iridium respectively, implying large investments by the mining industry.

However, the most critical element for the development of green hydrogen is the need for massive quantities of renewable electricity as water electrolysis is a very electro-intensive process. While renewable electricity capacity is growing fast, and this growth is expected to further accelerate, green hydrogen could be a large chunk of demand. In its net zero scenario, the IEA expects green hydrogen to consume 10% of the world’s electricity by 2050, from virtually zero today.

The consanguinity of green hydrogen and renewable electricity raises several issues:

- Crowding out: Renewable power used to produce hydrogen will not be available for other uses, in a context where renewable power is a key lever to decarbonise our economy

- Energy efficiency: Hydrogen is a relatively inefficient energy carrier given the energy required to produce and transport it. Direct electrification is a superior proposition to hydrogen and should be favoured whenever possible

- Application: Hydrogen is too-often hyped as a magic solution to all energy problems. Beyond greening existing production, it is important to ensure that new hydrogen production is dedicated to applications where there are no better alternatives.

We believe hydrogen will be best used to decarbonise heavy-duty, long-haul road transportation, long-haul shipping, steel making, and potentially certain industrial processes requiring very high heat. As it can be stored, typically in underground salt caverns, hydrogen could also play a role in managing power grids where intermittent sources will be dominant.

In addition, competing technologies must be monitored. For instance, progress in battery technologies could change the attractiveness of hydrogen in certain applications

Opportunities for investors

A hydrogen economy would have the advantage of being local – wherever there is wind, sun and water – and could help to reduce dependency on imported fossil fuels. Although it appears that water availability is not a technical and cost roadblock – with brackish or sea water desalination as a credible alternative to freshwater in water stressed regions – it could easily be more challenging to gain social acceptance at local community level.

More broadly, the overall acceptance and the risk perception of hydrogen are important factors to take into account. Its chemical nature means it ignites easily and is prone to leaks, and it is complex to handle along existing value chains thanks to the need for high compression and/or very low temperatures. There is a physical footprint to consider too, through the massive need for wind and solar farms.

We believe that investors should be very careful when assessing the opportunities and risks of the hydrogen space.

Renewable electricity is a clear and obvious route to gain exposure to the growth potential of green hydrogen. Greater use of electricity and the electrification of many processes promises decades of development for solar and wind power, and while we acknowledge that green hydrogen is one of many growth drivers, it also means that risks are spread. Electric utilities with strong credentials in renewables ought to benefit from the rise of the hydrogen economy.

We have seen that hydrogen is not an easy molecule to handle. As such, we believe companies already active in the production, and especially the logistics, of hydrogen – namely industrial gas producers – may have a competitive advantage. Their know-how in managing a complex value chain could set them ahead of would-be competitors, in our view. A few, mostly western, integrated oil and gas companies have started to invest in hydrogen. Their experience in complex energy value chains and chemical processes could make them credible hydrogen players, although they will primarily remain fossil fuel producers for many years.

Equipment providers may be an area where risks could trump the opportunities. Most notably, producers of electrolysis technologies are likely to see very strong volume growth, but also strong price pressures and sharp competition. We expect in time to see commoditisation arising for those selling the shovels and picks of the green hydrogen industry.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.