Why, and how, investors should integrate biodiversity into fixed income portfolios

Key points:

- Managing risks, having a positive impact and meeting regulations are three reasons why fixed income investors should consider biodiversity within their portfolios

- Biodiversity loss is a complex issue - active engagement and detailed sector and issuer-level analysis are required to tackle it

- Biodiversity must be considered as part of a holistic sustainable approach, as opposed to in isolation to climate change and social factors

One of the fundamental features of biodiversity is that it reaches into every part of our lives – and that means the impacts of biodiversity loss are felt across investment portfolios too. In our view there isn’t an asset class or sector that would not benefit from a close consideration of how those effects might change outcomes or affect financial returns.

When we look specifically at fixed income, we see important reasons why investors should begin to integrate biodiversity into their decision making.

First, biodiversity loss presents risks that could impact the performance of fixed income portfolios. As with climate change, the starting point is to understand the risks in play, divided into two components. They may be physical risks from biodiversity loss and ecosystem degradation, or transition risks linked to global efforts to tackle the problem, which include increasing liability risks.

We expect that companies which do not proactively address these risks, and which fail to adopt more sustainable nature-positive business models, could face higher costs or lower revenues, therefore reducing their ability to repay debt in the future.

- Nature-related physical risks – The dramatic degradation of biodiversity and of natural resources has created, and will continue to create, significant pressures on issuer supply chains and manufacturing processes. This in turn may lead to a loss of revenue or reduced profitability, ultimately impairing the ability of an issuer to repay its debt. Examples of this could include increased flood risks due to soil and flora reductions, difficulties sourcing raw materials, reduced suitability of land for crop cultivation, or costs incurred from forced relocations of manufacturing bases.

TNFD’s definitions of risks, Taskforce on Nature-related Financial Disclosures, retrieved March 2023 - For instance, the nuclear sector and the paper industry are among sectors responsible for large-scale water withdrawal, and often have their operations positioned close to water sources. Over time water availability may become a real operational risk for these industries. Many new nuclear facilities are built close to the sea, but existing inland sites will likely face water stress risks at some level.

Liquid assets: Why water stress should be a priority for responsible investors, AXA IM, December 2022 - Nature-related transition risks – Consumers are becoming more aware of the dangers of biodiversity loss and could shift their spending habits to products and services least associated with having negative impacts on nature. The shift could be more acute in the face of controversial events where a boycott of a company’s products occurs across a wide consumer base. In addition, issuers could face further risks from evolving regulation, technological breakthroughs, market changes, and litigation.

- A good example of liability-related transition risks is the case of US litigation around perfluoroalkyl and polyfluoroalkyl substances (PFAS) i.e., a large complex set of synthetic chemicals used in consumer goods. This litigation has given rise to new regulatory measures in both the US and European Union with a potential ban targeting these so-called ‘forever chemicals’. Another recent example would be the introduction of taxes on plastic packaging in some countries, like the UK, seeking to encourage intensive plastic users to adapt the company’s business model.

The UK plastic packaging tax came into force on 1 April 2022.

In our view, interactions between different categories of nature-related risks, in particular cascading interactions of physical and transition risks, could eventually lead to a nature-related systemic risk with consequences for global economies around the world.

Asset owners: The momentum builds

A second reason why we believe fixed income investors need to take action is that we can see increasing interest from asset owners who want to mitigate their negative impact on biodiversity by reducing the biodiversity footprint of their investment and financing activities. This rationale extends beyond pure financial performance and into ‘double materiality’ – the idea that investors should consider not only the impact the external environment has on a portfolio, but also the impact a portfolio has on the natural and social capital in the world.

This process can occur in two ways – by reducing the negative impact a portfolio has, or by identifying and supporting nature-positive solutions that have the potential to drive change within different sectors.

According to estimates from the Convention on Biological Diversity and the Intergovernmental Panel on Climate Change (IPCC), between $150bn-$440bn per year should be allocated to biodiversity solutions to reverse biodiversity loss.

(More) regulations are on their way

The Taskforce on Nature-related Financial Disclosures (TNFD) was established in 2021 and aims to help factor biodiversity into financial and business decisions by creating a framework for disclosure and for assessing risks, impacts, opportunities and dependencies. The TNFD’s complete recommendations are scheduled to be completed in September 2023 and will centre around the same four pillars as the Task Force on Climate-related Financial Disclosures (TCFD) – namely governance, strategy, risk and impact management, and metrics and targets.

Thankfully, many investors would be able to leverage on their experience with implementing requirements from TCFD when considering biodiversity and applying the TNFD framework. While the risks, metrics and targets may be different, the learnings around access to data and implementation within portfolios may be applied with similar governance frameworks. We believe, similar to the TCFD, that the escalation of TNFD-adoption may quickly filter through to mandatory reporting for many investors, requiring a greater understanding of the topic among all investors.

These are the three drivers working to put biodiversity centre stage: The risks are becoming ever more evident; large asset owners are starting to measure their impact and consider how to adapt portfolios; and this process is spurred on by approaching regulatory demands. The next question then, is how can biodiversity be successfully integrated into fixed income portfolios?

Assessing portfolio risks and impacts

The extent to which fixed income investors can consider biodiversity is determined by the availability of information from which they can make credible portfolio decisions. Data availability, quality and coverage are all crucial, as is what the data aims to show (e.g. risks to the portfolio, impacts of the portfolio, or alignment to future nature-related goals). The availability of biodiversity data isn’t perfect, and portfolio-level decisions should acknowledge this, rather than it being a hurdle to starting integration.

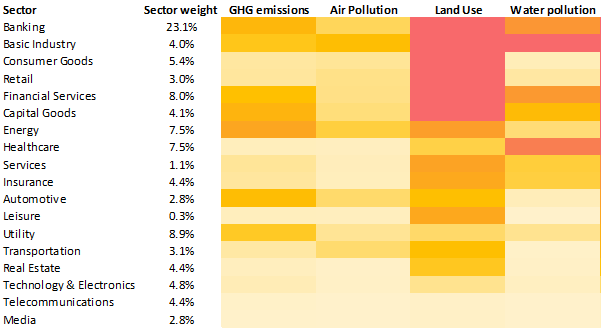

The heatmap below shows four of the primary drivers of biodiversity loss across the global investment-grade credit sectors, as measured with the use of the Corporate Biodiversity Footprint (CBF) metric provided by Iceberg Data Lab.

Picking out the biodiversity hotspots

Source: Iceberg Data Lab. Data as of 31/12/2022. For ease of illustration the CBF has been translated into a colour scale with the most impactful (red) having a score of about -0.2km2 MSA per million euros invested while the least impactful (light orange) having an MSA closer to zero.

One of the most striking findings is how heavily land use change contributes to overall biodiversity loss. The identification of land use change as the main pressure on biodiversity is in accordance with scientific consensus

Biodiversity as part of your investment process

After seeking out the portfolio ‘hotspots’ across sectors and specific issuers, investors can start the process of re-aligning their portfolio to reflect where best practice lies in biodiversity integration.

A basic starting point is to tilt portfolios away from issuers that have a high biodiversity footprint and little ambition to reduce it, towards companies in the same sector that have identified the risks and impacts and who are managing (reducing) and monitoring them. Detailed issuer-level analysis is critical here to assess the ambition and credibility of any corporate objectives.

Fixed income investors may also use the lever of bond maturities to mitigate biodiversity-related risks within their portfolios. For example, issuers with a high dependency on natural resources or a high biodiversity footprint could be invested in only at shorter maturities and only re-invested into upon maturity if they have made sufficient commitments to mitigate those risks or lower their footprint.

But what about managing this process of making changes to fixed income portfolios? While all investors can use portfolio inflows (and outflows) and active turnover to re-shape their strategies, fixed income investors also have the additional benefit of a certain portion of their portfolio maturing each year, often as much as 25% in short duration strategies. This natural turnover may give portfolio managers the choice of where to re-invest the proceeds to achieve their biodiversity goals in a cost-efficient manner to re-align their strategies to best practice in biodiversity integration.

The upcoming release of science-based pathways and sectoral guidelines, namely those expected to be provided by the Science Based Targets Network (SBTN), should further enhance the ability of corporates and investors to integrate biodiversity into their decision-making process.

Engaging with key sectors and issuers

Having a constructive dialogue and actively encouraging issuers to shift their business practices to reduce their biodiversity footprint is a key method to foster positive change. From a financial perspective it helps identify those ‘hotspots’ within a portfolio and structure discussions with issuers around material nature-related topics – helping them to become more aware of, and resilient to, the implications of supply chain and consumer risks from biodiversity loss. In other words, avoiding any surprises that might impair their ability to repay debt.

From an impact perspective that dialogue should encourage sustainable investors to take their share of responsibility by working closely with the investee companies to foster systemic change that can help to protect natural capital.

CASE STUDY – Biodiversity-specific projects in green bonds

Most bonds finance the general operating and capital expenditure of issuers. But use-of-proceeds bonds such as green, social and sustainability bonds can be directly linked to projects contributing to environmental or social objectives. There are currently no explicit ‘biodiversity’ bonds; however, several green bonds nod significant towards biodiversity. According to the 2021 Sustainable Debt Report by the Climate Bonds Initiative (CBI) at least 15% of the green sustainable debt use of proceeds under the analysis went to the land use, water and waste project categories in 2021.

The report also shows a slow but positive increase in land use project financing since 2014. AXA IM internal research comes to the same conclusions as regards the sustainability-linked bonds (SLBs) market, with 15%-18% of all the SLBs analysed in 2022 integrating nature-related targets, most of them focused on waste and water management.

In the current absence of clear trajectories on biodiversity, companies prefer to issue climate-oriented green bonds; therefore, a lot of nature-related use-of-proceeds bonds issuance comes from sovereign issuers.

Integrating biodiversity considerations into fixed income can be achieved through a range of tools and selecting green bonds with explicit biodiversity objectives as part of a wider green or traditional bond portfolio could materially contribute to this objective.

It is important to centre engagement around those sectors and issuers most relevant to the challenge at hand (see hotspots graphic). As with climate change, engagement on biodiversity loss can be extended from individual dialogue with companies to participation in collaborative initiatives such as Nature Action 100

It is possible that in some cases of engagement an issuer may be resistant to change their business practices, perhaps for fear of reducing profitability in the short run. Here a clear and established engagement framework and escalation process, which in extreme cases can even result in divestment, is critical to monitoring and implementing actions based on engagement activities.

Some might see divestment as the quickest way to reduce a portfolio’s biodiversity footprint, but it can have the counter-effect to a comprehensive and effective engagement strategy. In short, divestment means the investible universe is reduced and the point of contact and the potential leverage over the issuer is extinguished. With biodiversity-related data still maturing and financial institutions still building knowledge on the topic of biodiversity protection, an active engagement strategy may be better adapted than divestment for effectively tackling nature-related risks and identifying opportunities.

Where does biodiversity fit in relation to other sustainable investing?

Climate, biodiversity and social factors are inextricably linked. There is little value in pursuing improvements in one at the expense of the others. There are clear links, for example between climate change and biodiversity:

- Climate change is one of the five direct drivers of biodiversity loss – limiting climate change is therefore part of the solution for biodiversity erosion mitigation

- Natural capital and nature-based solutions, such as mangroves and forestry, not only represent high biodiversity-value areas but are also perfect carbon sinks which can help offset human-made carbon emissions

- Some climate change solutions may have important biodiversity impacts and contribute to biodiversity degradation. An example of this could be the building of a new dam. While providing clean energy, it can have significant impacts on the surrounding biodiversity ecosystems. A holistic assessment of environmental risks is therefore key for an effective transition to more sustainable economies.

When integrating climate change into investments, we think that a full lifecycle and value-chain analysis should be undertaken to consider the impact on biodiversity and on social issues related to economic activities. In general, the fundamental analysis undertaken should, at a minimum, be based on a ‘do no significant harm’ principle. This will allow positive progress to be made in each key area without damaging another.

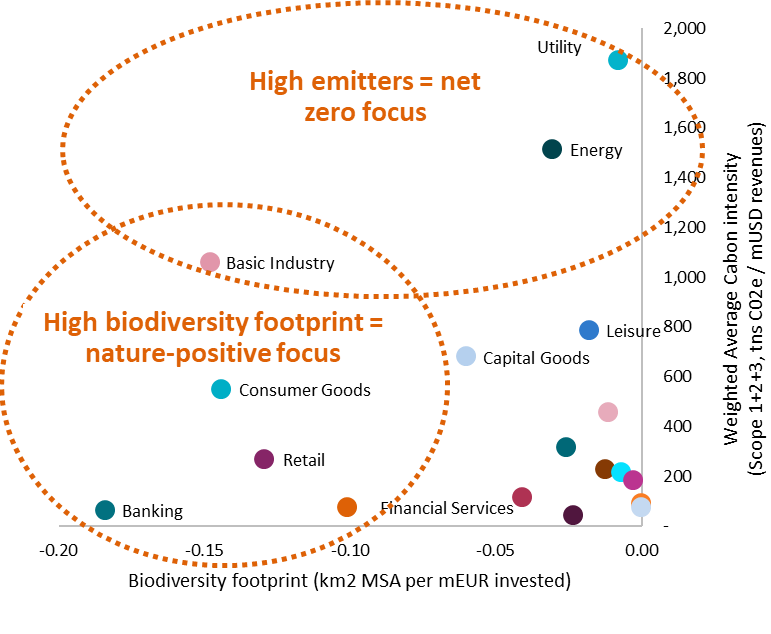

The chart below shows the degree of correlation between the weighted average carbon intensity (WACI) and biodiversity footprint (excluding climate change) across the global investment grade credit sectors.

The correlation between biodiversity loss and carbon emissions

Source: AXA IM, Trucost, Iceberg Data Lab, 31/12/2022

Clearly some sectors, such as basic industry, must tackle extensively both the climate change and biodiversity crisis together, while others can put their main focus on one or other, such as utilities (climate change) or consumer goods (biodiversity), but still apply minimum safeguards to avoid lateral environmental consequences.

In the same way that investors need to prepare for and consider a ‘just transition’ that weighs social impacts on the path to net zero, so biodiversity loss is another factor that must not suffer from investors’ carbon ‘tunnel vision’.

Fixed income investors can make a difference now

Biodiversity loss is rapidly rising up investors’ agendas due to the potential risks it can pose to their portfolios, the impact their investments have on the world, and because of upcoming regulations.

As a massive source of liquid capital, fixed income investors have a huge part to play in this emerging theme and can take steps today to actively improve the biodiversity footprint of their portfolios. We find that the running theme across implementation options is that an analysis must consider the full breadth of available data, but ultimately be driven by name and sector-specific fundamental analysis. Doing so allows investors to:

- Build internal knowledge and expertise on the biodiversity topic

- Identify and properly manage nature-related impacts, dependencies, risks and opportunities

- Determine the most appropriate engagement agenda and escalation tactics

By doing this, we think investors would be able to integrate biodiversity (and climate) in their portfolios in an efficient manner, potentially avoiding negative impacts on performance and positively contributing to returns at the same time as delivering long-term benefits to economies and people across the world.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2023 AXA Investment Managers. All rights reserved

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.