US Outlook – Second Term Trump

KEY POINTS

A new chapter

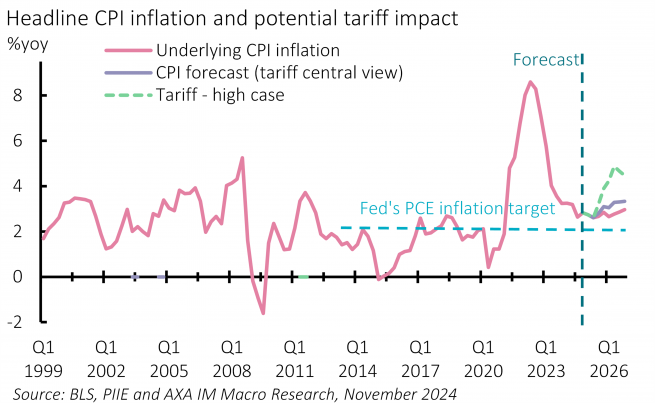

The US expanded by 2.8% annualised in Q3 2024 with consumption seeing a strong 3.7% rise. Although this followed weak headline expansion in Q1, due to dips in consumer and government spending as well as exports, Q2 was a robust 3.0% and 2024 as a whole looks set to deliver growth of 2.8%. However, despite growth’s robust pace, CPI inflation fell to 2.6% in October, around the pace consistent with the Federal Reserve’s (Fed) 2% PCE inflation target and marginally lower than we had anticipated last year (we forecast 2.9% for 2024 now, compared with 3.2% one year ago).

This combination of stronger growth and softer inflation largely reflected improving supply conditions: global supply chain tensions eased; labour market efficiencies improved, with vacancies falling more than unemployment has risen; and the labour supply increased, primarily from strong immigration. This has allowed the Fed to ease policy more quickly than expected and we expect one further 0.25% policy rate cut before year-end to leave the Fed Funds target at 4.25-4.50% as the Fed appears on track to delivering a soft landing.

Policy uncertainty replaces political uncertainty

If 2024 has played out a combination of recent years’ economic shocks and the Fed’s policy management, the coming years look more likely to be driven by the new administration’s policy direction. November’s election will return former President Donald Trump to the White House in 2025, with majorities in both houses of Congress. This was the result we expected

We are cautious of the growth outlook. Trump’s signature fiscal easing is likely to include a $4bn+ cost to extend the 2017 household tax cuts due to expire at the end of 2025. While the expiry would present a marked fiscal cliff, extending them merely maintains the status quo – it is not a stimulus. Corporate tax cuts to 15% (from 21%) would be different but even these are only small at 0.2% of GDP and previous tax cuts have rarely been shown to boost investment. Deregulation might prove more of a boost, particularly in gas production. But more broadly deregulation, which might extend to tech, AI and banking, typically provides moderate tailwinds, rather than one-off boosts. Even if the proposed Department of Government Efficiency does lift productivity (rather than just cut spending), this is unlikely to materialise in the first two years.

More fundamentally, further immigration restrictions and deportations would constitute a supply shock – limiting, or reversing labour supply growth – as would tariffs. Both are to be implemented to an uncertain scale but both would reduce US trend growth rates and boost inflation.

Two further uncertainties could also impair growth. While a full Budget is far from being prepared, the scale of tax cuts suggested is likely to see the deficit rise from its already elevated pace of around 6% of GDP per annum over the next 10 years. The Congressional Budget Office (CBO) currently estimates US debt exceeding 120% of GDP by 2034 and this could rise closer to 130% after Trump’s policies. This risks markets driving yields higher to incorporate a credit premium over coming years, with key risks if CBO deficits deteriorate further and the Treasury increases coupon issuance. Any such rise in yields would be a further headwind.

We are also mindful of geopolitical developments. Changing policies for Ukraine, the Middle East and increased economic tensions with China could topple the current, delicate geopolitical balance. We could not tell what new equilibrium might emerge but we are mindful that financial markets are rarely keen on uncertainty surrounding such transitions, something which may also dampen the growth outlook.

Growth to slow, inflation to rise

Our forecast is that with US activity enjoying solid momentum for now and a further loosening in financial conditions – in part in response to Trump’s win – the economy should post another solid year in 2025 and we forecast growth of 2.3%. However, as we expect the new administration to introduce growth restraining policies soon after inauguration, we expect growth to slow markedly across 2026, to leave annual growth at 1.5%, and annualised H2 2026 growth slower still.

Amid policy uncertainties, risks to our forecasts are two-sided. Growth could be supported beyond our expectations by a government efficiency drive, or a deregulatory spur to activity. But we do not assume full implementation of Trump’s supply shocks, which could impact the economy more. We are also wary of a rebalancing of geopolitical risks and the impact on financial conditions and growth.

While there is much debate over the growth outlook, we see fewer reservations over the outlook for inflation. The combination of boosting demand conditions and simultaneously restricting supply seems inevitable to deliver higher inflation. The question is again one of extent, given uncertainties surrounding the scale of policy implementation. The Peterson Institute estimates

Less space for monetary policy easing

We consider these developments likely to restrict the Fed’s space for monetary loosening, certainly relative to its September projections that saw the median (upper bound) Fed Funds forecast at 3.50% by end-2025 and 3.00% by end-2026. Indeed, we consider the Fed’s aggressive initial policy easing to have reflected a rebalancing of risks, trading off reduced downside growth/upside unemployment risks now for modestly above target inflation in the future. We still expect the Fed to ease policy to 4.50% by end-2024, but then consider just one more cut in 2025 to 4.25% in March, before supply shock policies raise the Fed’s inflation outlook. Longer term, based on our assessment that growth will start to slow in 2026, we expect the Fed to cut rates to 3.50% by end-2026. However, our expectation for the near term is for government policy to limit the Fed’s easing cycle. We also expect the Fed to end its quantitative tightening programme in the latter half of 2025.

There are wider concerns over the Fed’s independence under Trump. Both the President and Vice President-elect have suggested the President should have some say over policy. But recently Trump has said he does not want to mandate Fed actions but simply wants the right to comment on them. Trump has also suggested he would let Fed Chair Jerome Powell serve his term until 15 May 2026. This should allay concerns that Trump would remove Powell – something we suggest is legally trickier than it sounds. However, the Fed may still feel Trump’s ire if it ends its easing cycle in response to government policy.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.