The risk of lower US returns

Markets have largely ignored risks this year and delivered strong returns. But this has come at the expense of deteriorating valuations, especially in the US. Valuations themselves do not cause bear markets and the fundamental US macroeconomic backdrop remains supportive. However, the presidential election is next week, and market volatility is increasing. There is less valuation cover for investors than was the case a few months ago. It is only prudent that investors consider what might go wrong if risk-aversion continues to rise in response to something other than “Goldilocks” emerging on the macro front. The UK budget, and the market’s response, is perhaps evidence of just how fragile market confidence can be. On the positive side, seasonally, November tends to be a good month for risk (the dot.com crash of 2000 and the financial crisis of 2008 being the exceptions in recent US election years).

Expensive

A reasonable description of a bear market is when equities and credit generate returns well below those of less-risky assets like government bonds. In 2024 equity and corporate bond returns have outpaced returns from government bonds by healthy margins, making it a bull market year. In the US, strong growth (2.8% annualised GDP growth in Q3), has supported corporate profits while expectations of lower rates have helped companies manage their interest expenses. However, this has come at the cost of increasingly expensive valuations. The price-to-earnings (PE) ratio of the S&P 500, based on 12-month forecasts of earnings per share, is currently at 21.6 times according to the IBES Consensus. The average has been 16 since 2008. High yield credit spreads are tight. The asset swap spread on the ICE BofA US High Yield B-rated index is around 311 basis points (bp) which is in the bottom 7% of the distribution of that spread since 2014. Given we do not know what the post-election period will bring in the US, it is worth assessing how close we are to a bear market in risk assets, or at least to a period of returns being disappointing relative to the outcome in 2024 so far.

Catalysts for weaker markets?

A re-pricing of risk assets would need a catalyst. This could be a shock from policy or a derating of growth prospects (i.e. an increased risk of recession). The economy looks to be far away from recession but what the reaction could be to different policy decisions is unknown. Recessions can appear quite quickly. In the four quarters prior to each of the National Bureau of Economic Research (NBER) dated US recessions since 1964, GDP growth averaged between 3.5% and 4.0%. Markets could also react negatively to uncertainty in the immediate aftermath of the election if there are any disputed outcomes, or to an aggressive policy agenda (tariffs, aggressive tax cuts, attempted interference with monetary policy – and all have been suggested as potential policies under a Donald Trump administration).

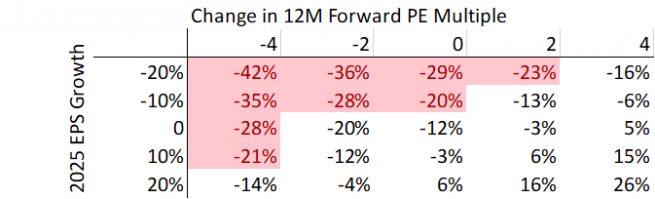

Earnings key to equity valuations

Typically a true bear market in equities occurs when prices fall by 20% from their highs. To get such a move in the S&P 500 from current levels would require a decline in the earnings multiple of around three-to-four percentage points. Such a move was seen in 2022 amid the first few months of monetary tightening, so it is not entirely out of the question. Or it could come about through a downward revision to earnings forecasts. The current consensus forecast for earnings growth over the next year is 13%. To get a 20% decline in the market earnings would need to decline by about 7% over the next year, assuming an unchanged multiple. Realistically it would be a combination of earnings and PE adjustment. Whatever caused earnings expectations to be reduced would encourage risk-off selling and a decline in the earnings multiple (and a consequent rise in the earnings yield). A halving of the 12-months earnings growth forecast and a decline in the PE multiple of three points would deliver a 20% decline in the S&P 500. Not that difficult to imagine, is it?

The S&P 500 earnings season is delivering a growth rate of around 9%, in line with expectations. In the technology sector, of the companies that have reported so far, most have met or beat forecasts on both sales and earnings. When there has been adverse share price movement, it has been on concerns about revenue expectations of certain businesses, or about costs involved in investing in data centres to further advance generative artificial intelligence capabilities. But, on the whole, the earnings profile looks healthy at the moment.

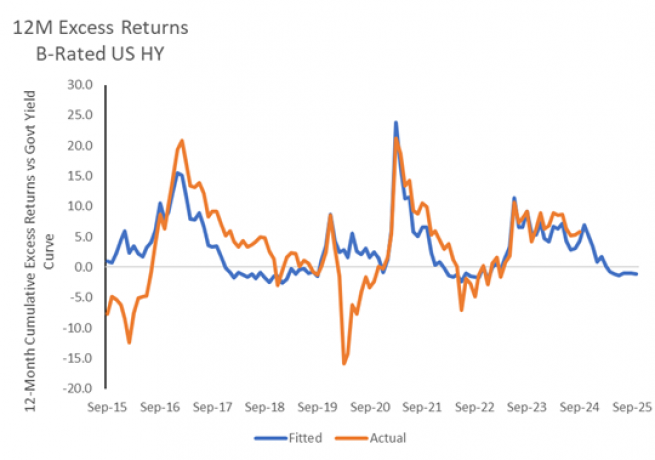

Spreads are not exciting

For high yield bonds the spread above the risk-free rate is the component of return that is meant to compensate for the additional risk of investing in the debt of leveraged and often highly-cyclical companies. The very minimum for a bear market in high yield would happen when spreads widened sufficiently to generate a lower return in high yield compared to less risky assets like US Treasuries (negative excess returns). The ratio of this spread to the duration of the asset is a good indicator of future excess returns. Based on current spread levels, it is likely that excess returns across high yield ratings buckets over the next year will be extremely low or even modestly negative. Again, it depends on what causes the widening of spreads but the point is that spreads offer little protection from investors experiencing negative excess returns over the next year.

The mitigation in high yield is to limit duration exposure and seek active management of high yield portfolios where good credit research can help avoid those issuers more likely to see rapid spread widening. Over the last 10 years the ratio of the asset swap spread to the duration of high yield indices has been 0.6 for the BB-rated index, 1.0 for the B-rated bucket and 2.7 for CCC-rated high yield bonds. Current ratios are below those averages for all three.

Into the red

Valuations themselves do not generate a bear market. However, they make investment returns more vulnerable to any change in underlying fundamentals (risk premiums are insufficient). It obviously remains important how the economy evolves in the months ahead. Growth has been strong, and inflation has been falling. This may remain the macro backdrop in which case a bear market would be low risk. However, one can build a worrying scenario based on potential policies that a Trump administration might enact. Bond yields have risen, which itself has raised the bar for risk assets. If the Federal Reserve is less able to cut rates because of fears that fiscal policy could provoke inflation, this could reignite recession concerns. I would argue that 10-year Treasury yields are close to fair value at current levels but that is based on the view that real yields can remain below the levels they were at prior to the financial crisis. If real GDP remains strong and there are growing fiscal concerns, real yields may need to go higher, pushing nominal yields to 5% or above. That could be a trigger for a bear market.

Investors need to consider different scenarios. This year has been rewarding - but it has been associated by narratives around risks. The US election has been one of those key risks alongside geopolitical events. The lack of materialisation of these risks on market performance combined with easier monetary policies has benefitted investors. Now, valuations are less helpful, markets have re-adjusted their most optimistic soft-landing scenarios for interest rates and the risks around the election and world events are still there. I would put a higher probability on returns not being as good in 2025 compared to this year.

And if?

Should riskier assets re-adjust to high valuations and worsening fundamentals, what would be the alternatives? On the fixed income side, a diversified flexible strategy that uses duration to offset any widening on the credit side would be attractive. As would short-duration strategies where the spread to duration ratio is less concerning. Given the lower valuation of European and Japanese equities, they may be more attractive than the US should US-centred risks materialise after 5 November.

Red box opened

Fiscal policy is now seen as a bigger risk to markets than monetary policy and the UK illustrated that this week. The UK budget statement, delivered by Chancellor Rachel Reeves, suggests higher taxes, higher government spending and more borrowing. The market has quickly hit back with higher bond yields. It’s not quite Liz Truss levels of market meltdown yet but the response of the gilt market will be a concern for the new Labour government as it implies fears about inflation – from higher public spending; weaker jobs growth – from the increase in employers National Insurance contributions; and debt stability if the extra spending does not translate into faster GDP growth. It was a progressive budget which favoured public services and disfavoured owners of assets, especially when those assets are earmarked for being passed to future generations. As such, the political flack is to be expected. What the long-term impact on the UK economy will be remains to be seen. In a global context however, the UK is not in that bad a position fiscally (certainly in comparison to the US). As such, I think gilts are looking to be offering decent medium-term value at these yield levels, especially as the Bank of England will still be reducing interest rates (even if not quite as much as was expected before the budget).

The spread between 10-year gilts and Treasuries reached 50bp after the Liz Truss budget. Today it is at 18bps.

Déjà vu reds

It is an unpleasant fact that if, in one’s professional life, you are not meeting your performance targets you may pay the ultimate price. In football, those performance targets are demanding (win more than you lose) and at a club with Manchester United’s history, they’re very demanding. Erik ten Hag became the latest manager to be seen to be failing to meet those targets. Replacing the coach is no guarantee that results will improve, but owners of football clubs have few choices when things are not going well. So, another era begins (5-2 is a good start) and the list of managers that have not lived up to Sir Alex Ferguson grows (maybe Ruud would?). For fans there is only one thing to do; deep intake of breath and fire up the hope once again.

(Performance data/data sources: LSEG Workspace DataStream, Bloomberg, AXA IM, as of 31 October 2024, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.