Take Two: Stocks reach another fresh high; Eurozone economy grows moderately

What do you need to know?

Rallying technology stocks drove the S&P 500, Nasdaq and Japan’s Nikkei 225 indices to new highs last week. However, US annual inflation reached a three-year high of 3.8% in April, from 3.3% in March, as the Iran war pushed up oil prices. Core inflation – excluding food and energy prices – increased to 2.8% from 2.6%, dampening expectations of US interest rate cuts. Meanwhile the International Energy Agency warned that global oil inventories are depleting at a record pace, as the Middle East war continues to impact supply.

Around the world

The Eurozone economy expanded moderately in the first quarter of 2026 as higher energy costs and geopolitical uncertainty weighed on momentum. The bloc’s GDP grew by 0.1%, according to a flash estimate, slower than the 0.2% growth in the previous quarter. The UK economy also grew in Q1, at a faster than anticipated rate of 0.6%, compared to Q4’s 0.2% growth. Elsewhere, China’s annual consumer price inflation rose to 1.2% in April, up from 1% in March, while its producer price index advanced to 2.8% from 0.5% in March, the fastest pace since July 2022.

Figure in focus: 50 billion tonnes

Some 50 billion tonnes of sand is used every year to meet growing infrastructure demand but is being extracted faster than nature can replenish it, according to a United Nations report. Sand is turned into concrete, asphalt, glass and more, and sand demand for buildings alone is expected to rise by 45% by 2060. However, left in its natural ecosystems, sand sustains biodiversity, filters water and buffers coastlines from erosion, amongst other important functions. Unsustainable extraction threatens ecosystems and livelihoods globally, the UN warned, though intervention remains possible.

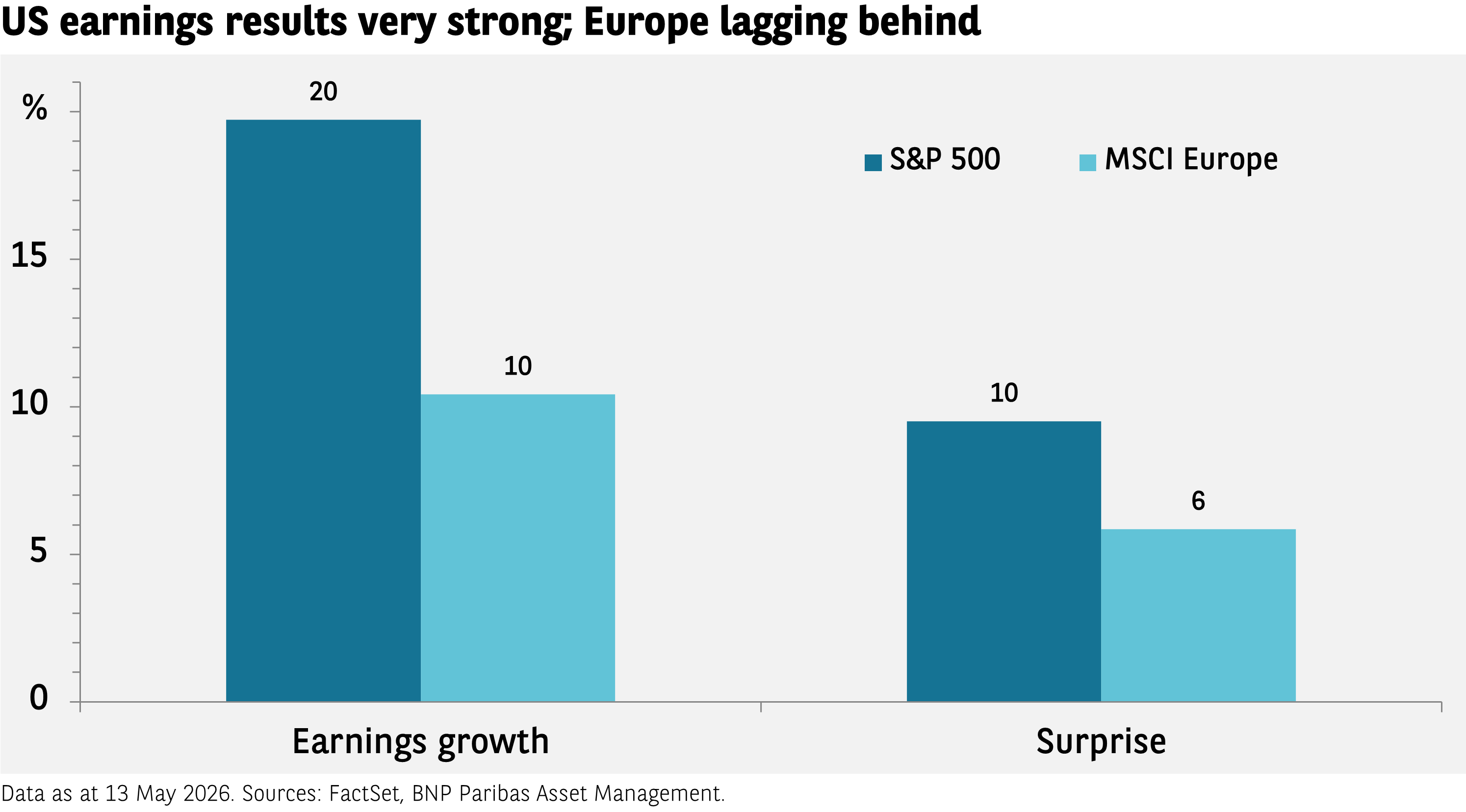

Chart of the week

The Q1 earnings season is wrapping up and results have far exceeded expectations, particularly in the US. For the S&P 500, earnings have risen 20% versus the same period a year ago. While technology companies’ earnings rose strongly, as expected, there was also solid growth across all sectors of the market. “Surprises”, that is, how much better the results were compared to forecasts, came to 10%; typically, the figure is 3%-4%. Results in Europe were still good but behind the US. Profits rose at half the rate and were very dependent on just two sectors: financials and energy. The results were nonetheless notably higher than expected.

Words of wisdom

Most: Scientists have uncovered a potentially cheap and emissions-free way of supplying heat which could be made available anywhere on earth. Molecular solar thermal – known as ‘Most’ – technology uses molecules which can be engineered to change shape when exposed to sunlight, allowing them to store energy for long periods. The molecules then release the energy when they revert to their original shape. However, several challenges remain, including the methods used to retain and transfer energy as currently these molecules can only be stored in liquid form, meaning complex pumping systems are necessary for the process.

What’s coming up?

On Tuesday, Japan issues a preliminary estimate of Q1 GDP growth, while the UK publishes unemployment data and Canada reports its latest inflation rate. On Wednesday, the UK and the Eurozone follow with April inflation data, and the US Federal Reserve releases the minutes of its latest monetary policy meeting. Thursday sees several flash Purchasing Managers’ Indices published including those covering Japan, the Eurozone, UK and US. On Friday, Japan updates markets with inflation data and Germany publishes a preliminary estimate of Q1 GDP growth.

Read more insights at the Investment Institute

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of BNP PARIBAS ASSET MANAGEMENT Europe or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.