LDI vs CDI: What are the portfolio implications?

KEY POINTS

Managing liabilities, securing long-term cashflows, and navigating market volatility are permanent questions for institutional investors. Not only will needs evolve over time but extreme market stress – such as that experienced in the UK in 2022 following Liz Truss’ mini budget and the subsequent bond market turmoil - can also impact institutional investor’s approach. The majority of pension funds or insurance providers will implement outcome-orientated solutions to help manage the specific risks they face.

Two of these solutions are LDI (Liability-Driven Investment) and CDI (Cash-Driven Investment), which are used by institutional investors in order to seek to achieve specific outcomes while catering to different financial objectives and risk profiles. As this market has evolved and expanded to meet client needs, several misconceptions about what LDI and CDI do have appeared:

Myth 1: You can only use one strategy or the other – not both

Although the acronyms ‘LDI’ and ‘CDI’ may sound alike, and have a focus on risk reduction, their objectives are different: As its name suggests, the objective of LDI is to hedge the interest rate and inflation sensitivities of liabilities to mitigate funding level volatility. This is typically achieved through utilising high-quality and liquid assets, typically in the denomination of the assets. Derivatives may be used to provide liquidity and leverage.

Conversely, a CDI portfolio’s primary focus is to pay the required cash payments through the natural income the portfolio receives from bond proceeds. The need to be able to provide cash when it is required leads to assets which give income with a higher degree of certainty such as investment grade credit. Due to the cost of buying and selling credit, leverage is not typically employed.

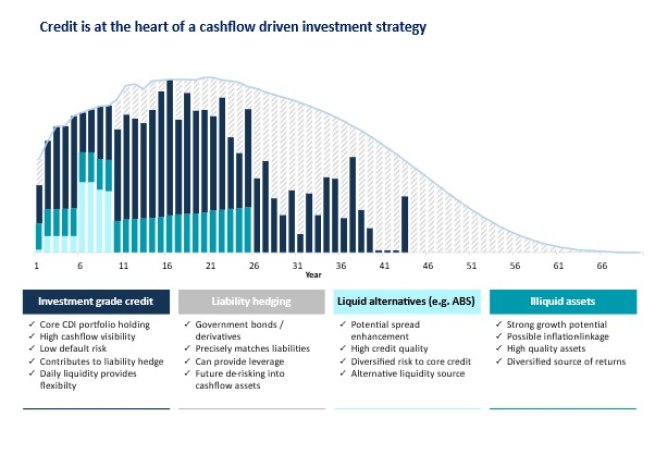

Taking these differences into account, it becomes clear that investors could utilise both an LDI portfolio, for hedging liabilities, and a CDI portfolio – for matching cashflows – the two are not mutually exclusive. In fact, a CDI portfolio can be a helpful addition for clients with an existing LDI portfolio, thanks to the interest rate exposure it provides which should help de-lever and diversify LDI exposure.

The diagram below shows how both strategies, alongside a broader mix of asset classes, can be combined to try to meet institutional investor needs.

Myth 2: Both require the same investment skill-sets

While there are many similarities, as Myth 1 describes, there are also some major differences in the tools used to implement these strategies which means the skills required of the manager are different too. As a clear example, the LDI focus on sovereigns and precise matching leads to the ability to precisely hedge a liability cashflow and manage collateral and liquidity due to leverage. By contrast, CDI strategies would have a much higher weight to credit and therefore credit research and risk management, as well as the ability to trade credit at scale, both on the primary and secondary markets, are key skill sets. To put some figures on the number of issuers to be monitored from a credit/issuer-risk perspective – LDI portfolios will often only hold one or a handful of different issuers from sovereigns or quasi-sovereigns, while the global credit universe has over 20,000 bonds from over 2,500 different issuers, each with their own specific risks.

We believe the above underscores the clear differences in the required skillsets between LDI and CDI managers.

Myth 3: They are low maintenance portfolios

While government bond and credit strategies are available, they are unlikely to meet the outcome-driven objectives of institutional clients to closely match liability exposures and to provide client-specific cashflows. In addition, ongoing risk monitoring and management is a crucial part of both LDI and CDI portfolios, albeit with the above-mentioned focus on different areas. Within credit portfolios, a Buy and Maintain approach – which focusses on the long-term fundamentals of issuers rather than short-term tactical trades - should help portfolios to adapt to changing market conditions as well as enabling other aspects such as sustainability to be built into the investment process. This is something which could not be so effectively implemented in a passive approach.

AXA IM’s partnership approach

Understanding the similarities and differences between LDI and CDI strategies is crucial for effective investment decision-making. While each represents holistic overall solutions, they require different skillsets.

When building an LDI or CDI strategy, we work closely with our clients and their consultants to ensure close collaboration between all parties, including, in the case of CDI portfolios, working with clients’ LDI managers to ensure a smooth onboarding and ongoing sharing of information, while also providing the benefits of a best-in-class fixed income manager.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.